Welcome back to MacroQuant Insights! Welcome back to another week of insightful economic updates. This week, we’re exploring key developments that have shaped the global economic landscape, from GDP revisions in the US to PMI data across major economies, let's unpack the numbers that matter!

🔍 Takeaway

This week’s economic data presents a complex picture, with strong GDP growth in the US, easing inflation in the Euro Area, and ongoing challenges in China’s manufacturing sector. Additionally, U.S. markets saw mixed performances ahead of the Labor Day holiday, with light trading volumes and significant movement in key stocks like NVIDIA.

United States: Strong GDP growth in Q2 at 3.0% reflects solid consumer spending and private investments, though the labor market shows signs of softening with steady unemployment claims and a hint of easing inflation, supporting the case for potential Fed rate cuts.

International: Canada’s GDP accelerates, driven by government spending and business investment, while Japan faces a rise in unemployment alongside steady consumer confidence. The Euro Area sees improved economic sentiment and a drop in inflation to 2.2%, suggesting progress toward the ECB’s target.

Emerging Markets: China’s manufacturing sector continues to contract, with the PMI slipping further into contraction territory. India’s economy grows at a slower 6.7% pace, reflecting resilience despite high-interest rates, while South Korea and Taiwan experience mixed performance, with South Korea seeing a decline in retail sales and Taiwan maintaining manufacturing growth.

⭐️ Post of the week

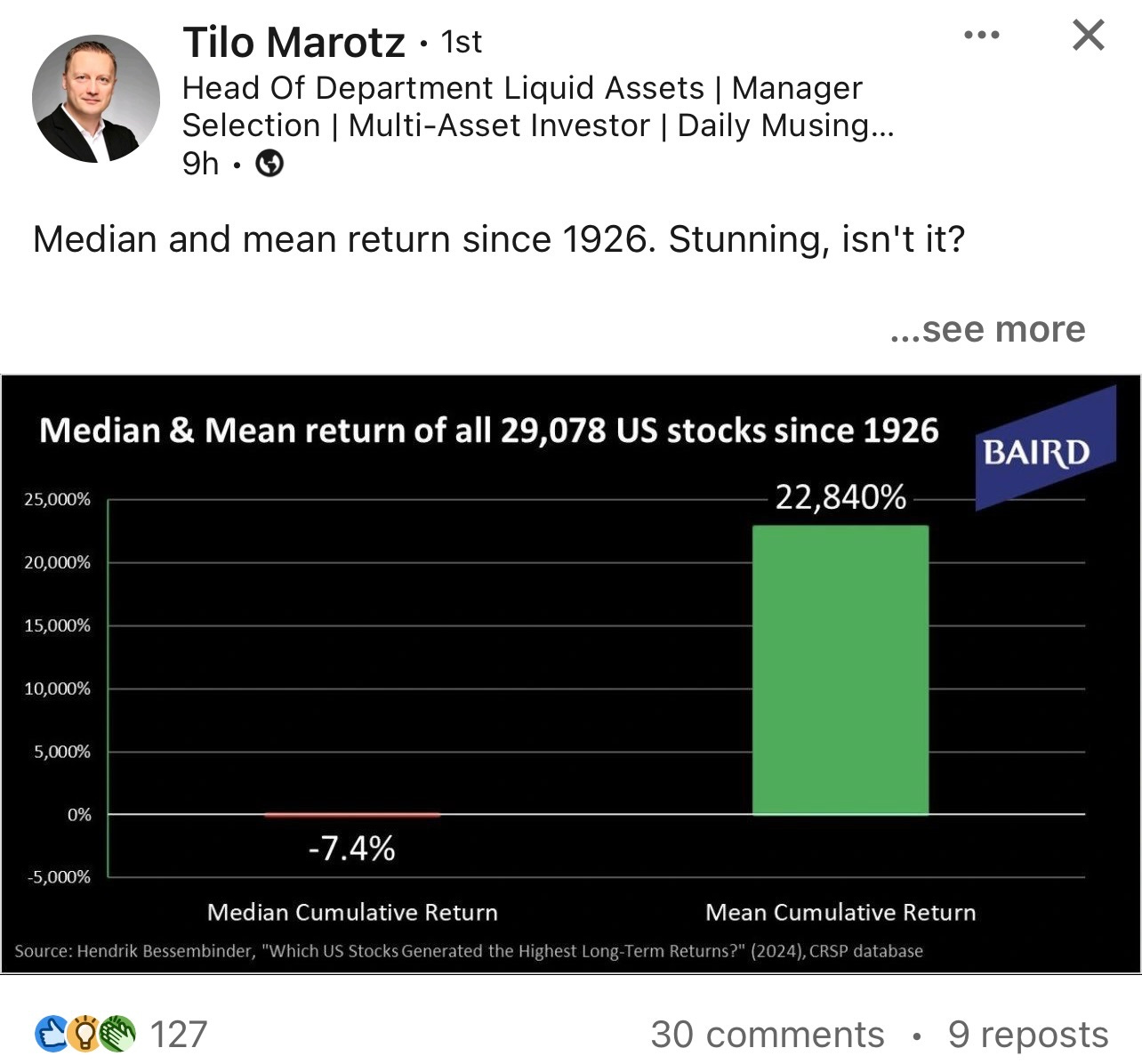

This week's post reveals a surprising contrast in US stock market returns since 1926. While the median cumulative return was -7.4%, the mean return was 22,840%. This huge gap shows that a small number of "superstar" stocks drove overall market gains, while most individual stocks actually lost value over time.

For investors, this data highlights the challenges and potential rewards of stock selection. It underscores the importance of thorough research and analysis when choosing individual stocks, as well as the potential benefits of maintaining a diversified portfolio. The study's 98-year timeframe also emphasizes the power of patient, long-term investing for wealth creation, showcasing how exceptional companies can deliver remarkable returns over extended periods.

Source: Tilo Marotz - LinkedIn

💼 Market Indicators

SPY Performance

Performance and Valuations by Region

Source: MSCI

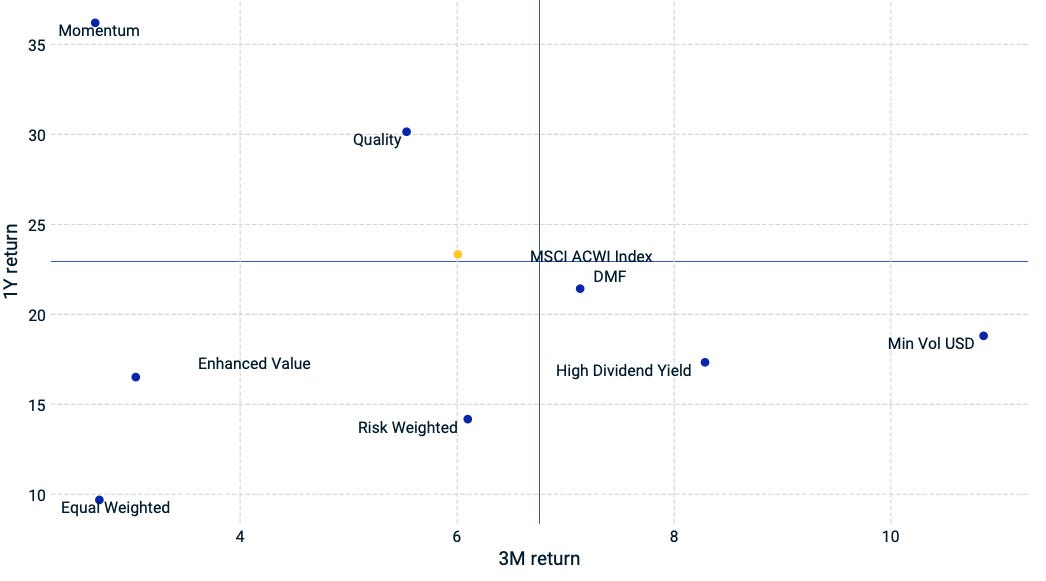

Momentum performance by Style

Source: MSCI

S&P 500 Earnings Per Share

Source: Yardeni Research

🇺🇸 United States: Growth Up, But Labor Market Softens

GDP Growth: US GDP was revised up to 3.0% for Q2 2024, driven by strong consumer spending (2.9%) and private inventory investment (7.5%). However, nonresidential fixed investment and exports were revised downward.

Labor Market: Unemployment claims slightly decreased to 231,000, while continued claims rose to 1,868,000, indicating a cooling labor market.

Inflation: Core PCE price index rose by 0.2% in July, in line with expectations, supporting the case for potential Fed rate cuts.

🌐 International: Mixed Economic Indicators Across Regions

🇨🇦 Canada:

GDP growth accelerated to 2.1% annualized in Q2 2024, driven by increased government spending and business investment, though household spending showed signs of slowing.

🇯🇵 Japan:

Consumer confidence held steady in August at 36.7, while the unemployment rate unexpectedly rose to 2.7%, highlighting concerns in the labor market. Retail sales growth slowed to 2.6% YoY in July, missing expectations.

🇪🇺 Euro Area:

Economic sentiment improved slightly to 96.6 in August, while inflation fell to 2.2%, the lowest since July 2021. The unemployment rate edged down to a record low of 6.4%.

🌏 Emerging Markets: Challenges in China, Resilience in India and Taiwan

🇨🇳 China:

The Manufacturing PMI fell to 49.1 in August, marking the fourth consecutive month of contraction, while the Non-Manufacturing PMI edged up slightly to 50.3, indicating modest expansion in the services sector.

🇮🇳 India:

The economy grew by 6.7% in Q2 2024, slowing from 7.8% in the previous quarter, with consumer spending showing resilience despite high-interest rates.

🇰🇷 South Korea:

Retail sales declined by 1.9% MoM in July, reversing gains from June, while the Manufacturing PMI softened to 51.4, indicating slower growth.

🇹🇼 Taiwan:

The Manufacturing PMI dropped slightly to 52.9 in July, still showing growth amid strong demand from Asia, Europe, and North America.

Stay tuned for next week's updates! Feel free to share your thoughts or questions below.