Weekly Economic Highlights

Week Ending August 17, 2024

Welcome back to MacroQuant Insights! This week, we’re diving into the most impactful economic events across the globe.

🔍 Takeaway

This week’s economic data shows slowing inflation in the US, mixed growth in developed markets, and persistent inflation in emerging markets.

United States: Inflation shows signs of easing, with core consumer prices moderating and retail sales rebounding strongly. However, building permits hit a four-year low, signaling potential weakness in the housing sector.

International: Japan's GDP growth surprises on the upside, driven by strong private consumption and business investment, while the UK experiences a decline in unemployment and a slight uptick in inflation. The Euro Area faces a downturn in economic sentiment, though GDP growth remains steady.

Emerging Markets: China’s industrial production slows, but retail sales pick up pace. South Korea's unemployment rate falls to its lowest level since October, reflecting a strong labor market.

⭐️ Post of the week

Source: Sébastien Page - LinkedIn

💼 Market Indicators

SPY Performance

Performance and Valuations by Region

Source: MSCI

Momentum performance by Style

Source: MSCI

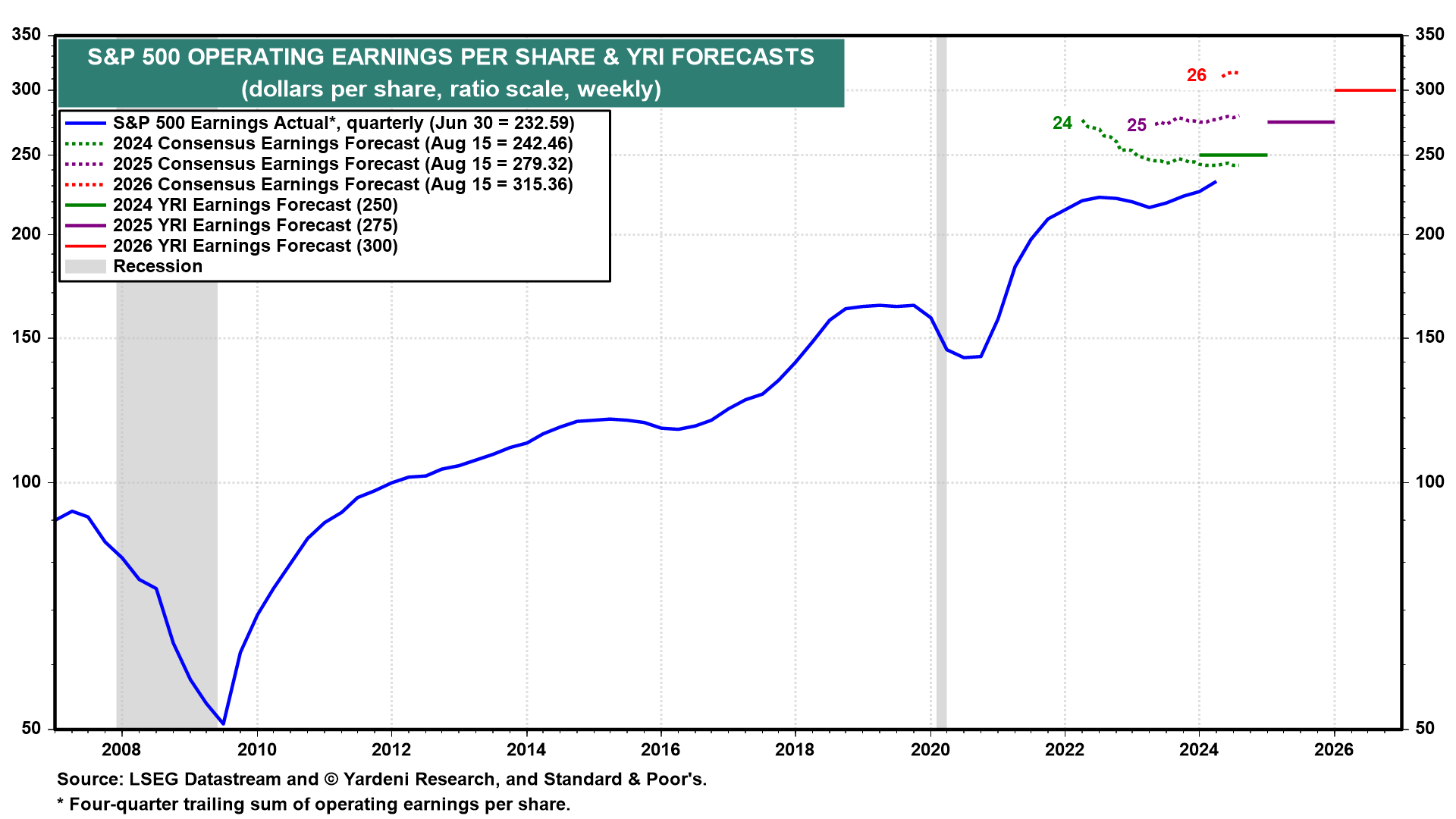

S&P 500 Earnings Per Share

Source: Yardeni Research

🇺🇸 United States: Continuing Disinflation Signals and Strong Retail Sales

Inflation: The annual inflation rate slowed to 2.9% in July 2024, the lowest since March 2021, with core inflation at 3.2%. Energy costs rose slightly, while prices for new vehicles continued to decline.

Producer Prices: Factory gate prices rose by 0.1% MoM, driven by energy costs, while core producer prices remained unchanged, easing YoY to 2.4%.

Retail Sales: Surged by 1% MoM in July 2024, the largest increase since January 2023, led by motor vehicle sales and electronics.

Building Permits: Fell by 4% to a four-year low of 1.396 million, with significant declines in multi-unit permits.

🌐 International: Diverging Growth and Shifting Economic Sentiments

🇨🇦 Canada:

Building Permits: Dropped sharply by 13.9% MoM in June 2024, led by declines in both residential and non-residential sectors.

🇯🇵 Japan:

GDP Growth: Expanded by 0.8% QoQ in Q2 2024, driven by strong private consumption and business investment, marking the highest growth since Q1 2023.

Producer Prices: Increased by 3.0% YoY in July 2024, the highest in nearly a year, with significant rises in transport equipment and chemicals.

🇬🇧 United Kingdom:

Unemployment Rate: Fell to 4.2% in Q2 2024, with a notable decrease in the number of unemployed individuals.

Inflation: Edged up to 2.2% in July 2024, with rising prices for housing and household services.

🇪🇺 Euro Area:

Economic Sentiment: The ZEW Indicator plunged to a nine-month low of 17.9 in August 2024, reflecting ongoing uncertainty and deteriorating economic outlook.

GDP: Grew by 0.3% QoQ in Q2 2024, with Germany unexpectedly contracting by 0.1% amid industrial challenges.

🌏 Emerging Markets: Varied Economic Performance

🇨🇳 China:

Industrial Production: Grew by 5.1% YoY in July 2024, slowing from the previous month, with notable declines in manufacturing and utilities.

Retail Sales: Accelerated by 2.7% YoY, driven by strong growth in communication equipment and sports & recreation articles.

🇰🇷 Korea:

Unemployment Rate: Dropped to 2.5% in July 2024, the lowest since October, with a significant increase in the number of employed persons.

Stay tuned for next week's updates! Feel free to share your thoughts or questions below.