Weekly Economic Highlights

Week Ending August 24, 2024

Welcome back to MacroQuant Insights! Welcome back to another week of insightful economic updates. This week, we’re diving into key developments from the United States, International markets, and Emerging Economies. From central bank signals to shifting market trends, let's unpack the numbers that matter!

🔍 Takeaway

This week’s economic data shows the Federal Reserve signaling potential rate cuts amid a cooling labor market, mixed inflation trends in developed markets, and persistent inflationary pressures in emerging economies.

United States: The Fed hints at a rate cut as inflation shows signs of easing, with the PMI data indicating slower growth in manufacturing and a softening labor market evidenced by rising unemployment claims.

International: Canada’s inflation cools, driven by lower shelter costs, while Japan’s services sector supports growth despite manufacturing struggles. The UK sees strong PMI growth, particularly in the service sector, while the Euro Area experiences a slight uptick in inflation, with steady economic activity driven by services.

Emerging Markets: India’s growth remains robust, however slightly slower, with South Korea experiencing rising producer inflation. Taiwan’s retail sales grow, though at a decelerated pace, with mixed performance across sectors.

⭐️ Post of the week

Source: James Bianco - LinkedIn

💼 Market Indicators

SPY Performance

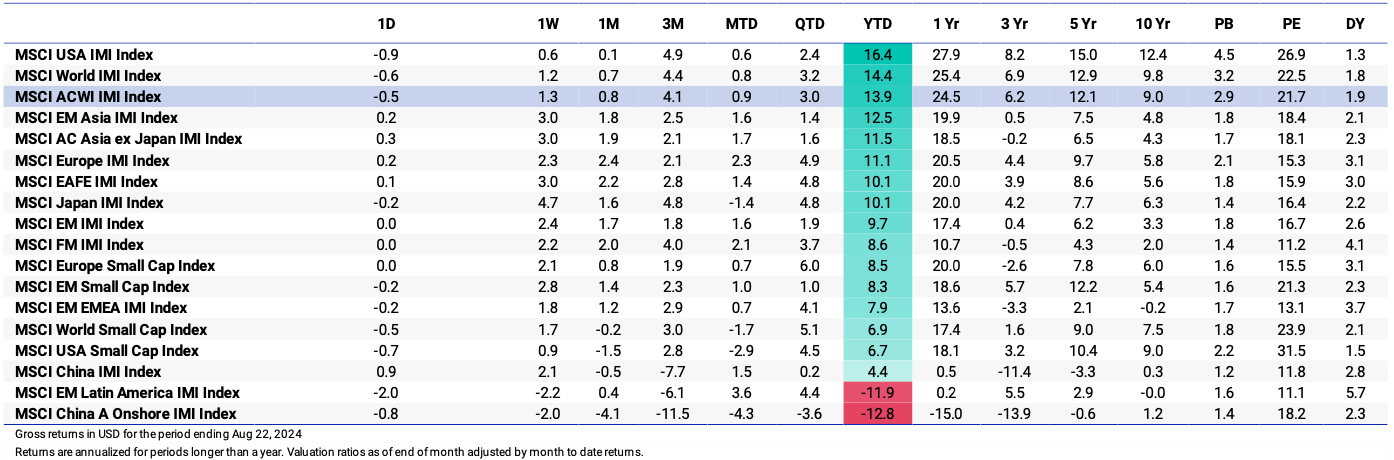

Performance and Valuations by Region

Source: MSCI

Momentum performance by Style

Source: MSCI

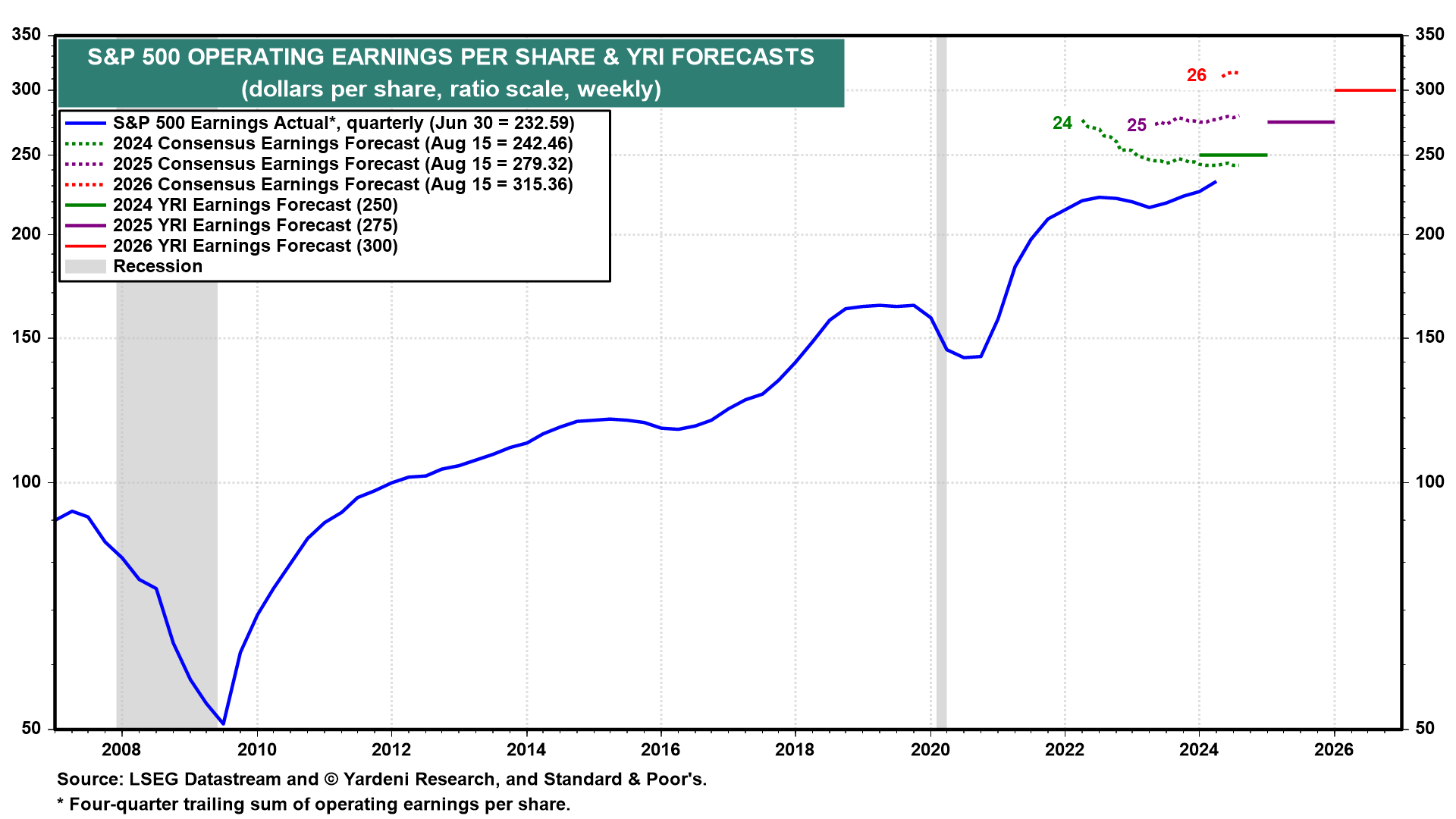

S&P 500 Earnings Per Share

Source: Yardeni Research

🇺🇸 United States: Cooling Labor Market and Fed Signals

Federal Reserve: Fed Chair Jerome Powell indicated a likely rate cut in September, citing a cooling labor market and inflation nearing the 2% target.

PMI Data: The US Composite PMI dipped slightly to 54.1 in August, still reflecting expansion but at a slower pace, especially in manufacturing.

Employment: Unemployment claims rose to 232,000, marking a three-week high, reinforcing the narrative of a softening labor market.

🌐 International: Central Bank Moves and Economic Indicators

🇨🇦 Canada:

Inflation: Eased to 2.5% in July, marking the slowest increase since March 2021, driven by lower shelter costs and stable transportation prices.

Retail Sales: Increased by just 0.2% YoY in June, the smallest gain in five months, signaling weaker consumer spending.

🇯🇵 Japan:

PMI: Composite PMI rose to 53.0 in August, the highest since May 2023, led by the services sector, despite continued manufacturing shrinkage.

Inflation: Held steady at 2.8% in July, with electricity and gas prices spiking as government subsidies ended.

🇬🇧 United Kingdom:

PMI: Composite PMI rose to 53.4 in August, driven by strong service sector growth and increased employment, despite ongoing inflationary pressures.

🇪🇺 Euro Area:

Inflation: Edged up to 2.6% in July, with energy costs rising sharply, maintaining pressure on the ECB's monetary policy.

PMI: Composite PMI increased to 51.2 in August, indicating continued but uneven growth, with services expanding and manufacturing contracting.

🌏 Emerging Markets: Varied Economic Performance

🇮🇳 India:

PMI: Composite PMI ticked lower to 60.5 in August, reflecting strong but slightly slower growth in private sector activity.

🇰🇷 South Korea:

Producer Inflation: Increased to 2.6% YoY in July, driven by rising manufacturing and energy costs, despite stable service prices.

Interest Rates: The Bank of Korea held its base rate steady at 3.5%, citing conflicting economic signals and concerns over household debt.

🇹🇼 Taiwan:

Retail Sales: Rose by 3.4% YoY in July, though growth slowed from the previous month, with significant declines in textiles and clothing sales.

Stay tuned for next week's updates! Feel free to share your thoughts or questions below.