Welcome back to MacroQuant Insights! Welcome back to another week of insightful economic updates. This week, we’re diving into the most impactful economic events across the globe, from the cooling labor market in the U.S. to central bank policy shifts in Canada and Japan. Let’s unpack the key data driving market moves and macro trends this week.

🔍 Takeaway

This week’s economic data presents a complex picture, with concerns over a weakening U.S. labor market, improved inflation in the Euro Area, and persistent struggles in China's manufacturing sector. Additionally, U.S. markets experienced their steepest drop in 18 months as investors braced for potential economic slowdowns.

United States: The S&P 500 posted a 4.9% decline, its worst weekly performance in 18 months, as concerns over NVIDIA’s potential antitrust investigation and a slowing economy weighed on markets. Job openings fell to 7.67 million in July, the lowest level since January 2021, signaling a cooling labor market.

International: Canada’s trade surplus returned in July, driven by a drop in imports. The Euro Area saw easing inflation, with producer prices dropping 2.1% YoY, while Japan’s economy continues to recover, supported by strong consumer spending.

Emerging Markets: China’s manufacturing sector contracted further, with the PMI slipping to 49.1, while India’s economy maintained growth at 6.7% despite high interest rates. Taiwan saw slowing manufacturing growth, but inflation eased slightly to 2.36%.

⭐️ Post of the week

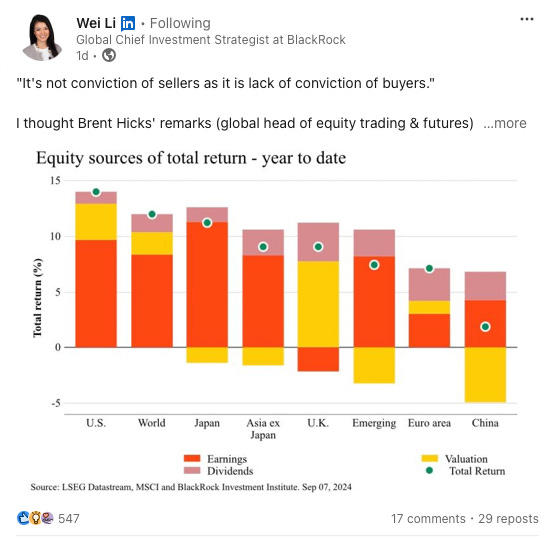

This week's chart highlights the regional disparity in equity market returns year-to-date, showcasing how earnings and valuation shifts have driven performance. While the U.S. posted strong returns, China remains an outlier with low returns driven by significant valuation declines.

For investors, the data emphasizes the importance of understanding the different drivers behind market returns. Relying solely on earnings growth might not capture the full picture, especially in markets where valuation changes or dividends play a more significant role. This insight is particularly relevant when evaluating regions like China, where valuation declines have led to negative returns despite earnings and dividend contributions.

Source: Wei Li - LinkedIn

💼 Market Indicators

SPY Performance

Performance and Valuations by Region

Source: MSCI

Momentum performance by Style

Source: MSCI

S&P 500 Earnings Per Share

Source: Yardeni Research

🇺🇸 United States: Cooling Labor Market and Fed's Watchful Eye

Fed Watch: Federal Reserve Chairman Jerome Powell signaled a likely rate cut in September as the U.S. labor market cools, aligning with inflation trends nearing the 2% target.

Job Openings: Fell to 7.673 million in July 2024, the lowest since January 2021, reflecting softening demand in key sectors.

ISM Manufacturing PMI: Remained in contraction territory at 47.2 in August, marking the 21st monthly decline in 22 months.

Employment Growth: The economy added 142K jobs in August, missing expectations and signaling a slowdown in growth.

🌐 International: Central Bank Moves and Economic Adjustments

🇨🇦 Canada:

Trade Surplus: Canada posted a CAD 0.68 billion surplus in July 2024, driven by a drop in motor vehicle sales and imports.

BoC Rate Cut: The Bank of Canada cut its key interest rate by 25bps to 4.25%, marking the third consecutive cut as the labor market continues to slow.

🇯🇵 Japan:

Manufacturing PMI: Rose to 49.8 in August, nearing stabilization, as output improved and inflationary pressures mounted.

GDP Growth: Japan’s economy grew by 3.1% in Q2 2024, buoyed by robust consumer spending and wage increases.

🇪🇺 Euro Area:

GDP Growth: Grew by 0.6% YoY in Q2 2024, driven by government spending and a drop in imports.

Producer Prices: Decreased 2.1% YoY in July, with energy and intermediate goods prices continuing to decline.

🇬🇧 United Kingdom:

Retail Sales: Retail sales increased by 0.8% YoY in August, boosted by warm weather driving clothing and food sales.

Composite PMI: Rose to 53.8, reflecting expansion in services and manufacturing, with smaller input cost increases since 2020.

🌏 Emerging Markets: Mixed Signals in Growth and Inflation

🇨🇳 China:

Manufacturing PMI: Improved to 50.4 in August, signaling growth in new orders and production despite weakening export demand.

Inflation: Rose to 0.5% in July, marking the highest rate since February, with food prices stabilizing after months of decline.

🇮🇳 India:

HSBC Manufacturing PMI: Eased to 57.5 in August, though growth remains historically elevated. Business confidence fell amid rising inflation concerns.

🇰🇷 South Korea:

GDP: South Korea’s economy shrank 0.2% in Q2 2024, its first contraction since Q4 2022, driven by declines in private consumption and construction investment.

🇹🇼 Taiwan:

Manufacturing PMI: Fell to 51.5 in August, its softest level since May, as output growth slowed and shipping delays weighed on inventories.

Stay tuned for next week's updates! Feel free to share your thoughts or questions below.