U.S. stocks tumbled this week, with the S&P 500 shedding 3.2% in its worst performance since early September as uncertainty surrounding Trump's trade policies dominated sentiment. This selloff, fueled by the implementation deadline for 25% tariffs on Canadian and Mexican imports alongside an additional 10% on Chinese goods, came despite later exemptions and delays that failed to calm investor nerves. As manufacturing activity slowed to just 50.3 and new orders contracted sharply to 48.6%, the simultaneous spike in price pressures to 62.4% underscored the complex challenges now facing both corporate earnings and Fed policy in the months ahead.

⏱️ Global Markets in 10 Seconds:

🇺🇸 S&P 500 -3.2% worst week since September amid tariff fears 📉

🇨🇦 Manufacturing PMI 47.8 first contraction since August on trade anxiety 🏭

🇪🇺 ECB cuts rates to 2.5% as growth forecast drops to 0.9% 🏦

🇯🇵 10-year bond yield 1.53% highest since 2008 as deflation era ends 📈

🇨🇳 Fiscal deficit 4% of GDP highest since 1994 to counter trade headwinds 💰

🔍 The Big Picture

This week's market narrative centered around escalating trade tensions and their ripple effects across global economies. The deadline for Trump's tariff implementation rattled investors despite last-minute exemptions, while central banks navigated the delicate balance between inflation concerns and slowing growth trajectories.

United States: Talk about a split economy – services activity accelerated to 53.5 while manufacturing barely hung on at 50.3 with new orders plunging into contraction territory at 48.6. This divergence, combined with the jump in price pressures to 62.4%, suggests we're seeing the first economic casualties of the new administration's tariff policy, with the Fed's Powell now emphasizing they're in no rush to cut rates further amid this "phenomenal uncertainty."

International: The ECB's decision to cut rates to 2.5% while simultaneously slashing their 2025 growth forecast to just 0.9% reveals the precarious position Europe finds itself in. Meanwhile, Canada's manufacturing PMI collapse to 47.8 represents the sharpest contraction since December 2023, driven directly by cross-border trade anxiety. Japan's story adds another layer of complexity with 10-year government bond yields reaching 1.53% – their highest since 2008 – as the country prepares to officially declare the end of its decades-long deflationary era.

Emerging Markets: China's approach to countering trade headwinds shows a government willing to pull out all the stops, setting their fiscal deficit target at 4% of GDP (highest since 1994) while maintaining an ambitious 5% growth goal. Contrast this with Taiwan, where inflation eased considerably to 1.58% from 2.66%, creating potential monetary policy flexibility that China simply doesn't have. South Korea sits somewhere in between with inflation at 2%, allowing their central bank to cut rates while maintaining relative price stability – essentially giving us three distinct EM playbooks for navigating this increasingly turbulent global environment.

💼 Market Indicators

SPY Performance

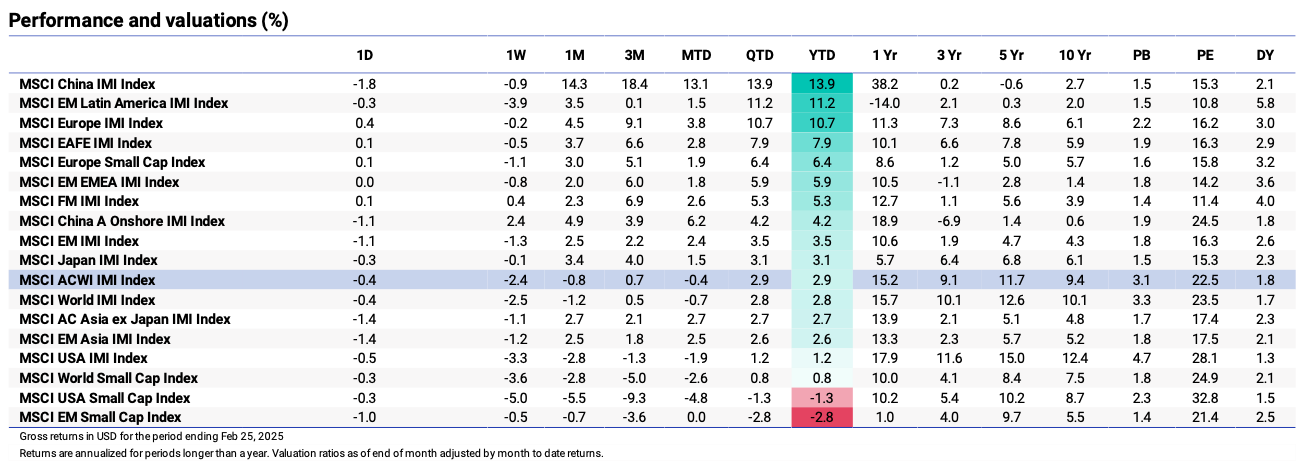

Performance and Valuations by Region

Source: MSCI

Momentum performance by Style

Source: MSCI

S&P 500 Earnings Per Share

Source: Yardeni Research

🗺️ Around the World in Detail

🇺🇸 United States: Sector Divergence

Manufacturing PMI slipped to 50.3 in February, barely hanging onto expansion territory while new orders plunged into contraction at 48.6. This is our first real economic indicator showing the impact of tariff policy uncertainty, with ISM specifically citing "the first operational shock of the new administration's tariff policy."

Services PMI surprisingly strengthened to 53.5, marking the third consecutive month with all four sub-indexes in expansion. Looks like the American consumer isn't too concerned about trade wars yet, though the ISM chair noted "anxiety continues" among survey respondents regarding tariff impacts.

Job growth increased to 151K in February from January's downwardly revised 125K, still missing expectations but showing labor market resilience. The interesting wrinkle? Federal government jobs declined by 10K, giving us an early taste of the promised spending cuts.

Unemployment ticked up to 4.1% while the U-6 underemployment rate jumped more significantly from 7.5% to 8.0%. That half-point jump suggests the headline numbers might be masking some deterioration beneath the surface.

🌐 International Markets: Policy Pivot

Canada 🇨🇦

Manufacturing PMI collapsed to 47.8 from 51.6, the sharpest contraction since December 2023. The culprit? Uncertainty around cross-border trade policy, with firms reporting clients have adopted a "cautious approach" – corporate speak for "we're terrified about tariffs."

Services PMI plummeted to 46.6, marking the third straight month of contraction at an accelerating pace. The synchronized decline across both sectors reveals just how dependent Canada's economy is on its southern neighbor, with businesses already pulling back before a single tariff has actually been collected.

Europe 🇪🇺

ECB cut rates by 25 basis points to 2.5%, describing policy as now "meaningfully less restrictive." When Christine Lagarde describes the current environment as having "phenomenal uncertainty," you know central bankers are sweating.

Growth forecast for 2025 was slashed to just 0.9%, reflecting the ECB's concern that trade uncertainty is already impacting investment and exports. The eurozone is caught in the crossfire of a trade war it didn't start but can't escape.

Japan 🇯🇵

10-year government bond yields surged to 1.53%, their highest level since 2008, as the government prepares to officially declare the end of deflation. After decades of fighting falling prices, Japan is about to close that chapter – a genuine economic regime change.

Unemployment rate edged up to 2.5% in January, slightly above expectations, while the jobs-to-applications ratio improved to 1.26 – its highest in nine months. This mixed labor picture complicates the Bank of Japan's rate path as they navigate the post-deflation era.

🌏 Emerging Markets: Divergent Strategies

China 🇨🇳

Fiscal deficit target was set at 4% of GDP, the highest since 1994, signaling Beijing's willingness to spend heavily to counter trade headwinds. When China breaks its longstanding 3% deficit cap, you know they're getting serious about stimulus.

Annual inflation climbed to 0.5% in January from 0.1% in December, suggesting recent stimulus measures might be starting to gain traction. Food prices finally rebounding after a prolonged slump offers a glimmer of hope for domestic consumption.

Growth target remained unchanged at 5% for the third straight year, a sign of confidence amid mounting challenges. The question remains: can China hit this ambitious target with tariffs rising and a property sector still in the doldrums?

South Korea 🇰🇷

Inflation rate eased to 2% in February from January's six-month high of 2.2%, creating space for monetary policy flexibility. This moderation follows the Bank of Korea's first rate cut, suggesting their policy pivot was well-timed.

The central bank maintained its inflation forecast at 1.9% for both 2025 and 2026, projecting confidence in their disinflationary trajectory.

Taiwan 🇹🇼

Annual inflation rate dropped dramatically to 1.58% in February from 2.66% in January, marking the lowest reading since March 2021. This sharp deceleration creates policy flexibility just when Taiwan might need it most given cross-strait tensions.

Food inflation edged higher to 3.98% from 3.72%, creating a potential pressure point for households despite the overall disinflationary trend. This divergence between headline and food inflation presents a classic policy dilemma for Taiwanese authorities balancing growth and stability.

🔑 Key Takeaway

This week's data spotlights the immediate economic shockwaves from Trump's tariff policy, creating a market environment defined by uncertainty across regions and sectors. The stark manufacturing/services divide in the U.S. (50.3 vs 53.5 PMI) mirrors the broader global pattern where trade-exposed sectors are already showing strain despite minimal actual tariff implementation to date. Canada's synchronized manufacturing and services contraction (47.8 and 46.6 respectively) serves as the canary in the coal mine, showing how rapidly trade uncertainty can infect broader economic activity. Meanwhile, central banks like the ECB find themselves navigating what Lagarde aptly called "phenomenal uncertainty," cutting rates to 2.5% while slashing growth forecasts.

The content provided on MacroQuant Insights is for informational and educational purposes only and does not constitute financial advice. While every effort is made to ensure accuracy and reliability, all data, analysis, and opinions are based on sources believed to be trustworthy but are not guaranteed for completeness or timeliness. The views expressed are solely those of the author and do not reflect endorsements or recommendations for any specific investment, strategy, or action.

Investing involves inherent risks, including the potential loss of principal. Past performance is not indicative of future results. We strongly encourage readers to conduct their own research and consult with a qualified financial advisor or professional before making any financial decisions. MacroQuant Insights and its contributors disclaim all liability for investment decisions based on the information provided and make no warranties regarding the content’s accuracy or reliability.

Remember, all investments carry risks, and it is essential to understand these risks fully before acting on any information presented. Users are responsible for their own investment decisions. MacroQuant Insights assumes no responsibility for any outcomes resulting from the use of this information. Content is subject to change without notice.