Global Markets Juggle Inflation, Growth, and Policy Shifts in a Pivotal Week

Week Ending November 15, 2024

Welcome back to this week’s global market recap! Markets worldwide navigated a complex landscape, from U.S. inflation ticking higher and European growth surprising to China battling persistent deflation. Meanwhile, the incoming Trump administration added layers of uncertainty to already volatile financial markets. Let’s unpack the critical economic trends shaping the outlook for investors.

🔍 Takeaway

This week’s macroeconomic trends highlight a world in transition. U.S. inflation persists, with shelter and transportation costs complicating the Federal Reserve’s path. Rising Treasury yields signal markets adjusting to prolonged higher rates, pressuring growth sectors. Europe shows resilience in GDP but remains fragmented, while China struggles with deflation despite hints of stabilization in retail and housing. Investors face a delicate balance between inflation, uneven growth, and shifting policies.

United States: Inflation pressures persist, with headline CPI rising to 2.6% and core inflation steady at 3.3%, driven by shelter costs. Retail sales beat expectations, growing 0.4% in October, but Powell’s comments signaled no urgency to cut rates. Rising 10-year Treasury yields, now at 4.51%, reflect a higher-for-longer environment, posing challenges for equities while supporting income-focused strategies.

International: The Eurozone avoided recession with 0.4% GDP growth in Q3, but Germany’s economy remains fragile with only 0.2% growth. In the UK, GDP grew by 0.1%, while unemployment hit 4.3%, reflecting broad economic challenges. As the ECB signals caution, selective opportunities may arise in equities tied to fiscal support and regional growth.

Emerging Markets: China’s economy shows mixed signals, with retail sales up 4.8% but deflation in producer prices deepening. Housing declines eased slightly, yet broader property challenges persist. Meanwhile, India’s inflation jumped to 6.21%, breaching policy thresholds. Short-term opportunities exist, but structural risks demand caution.

⭐️ Post of the week

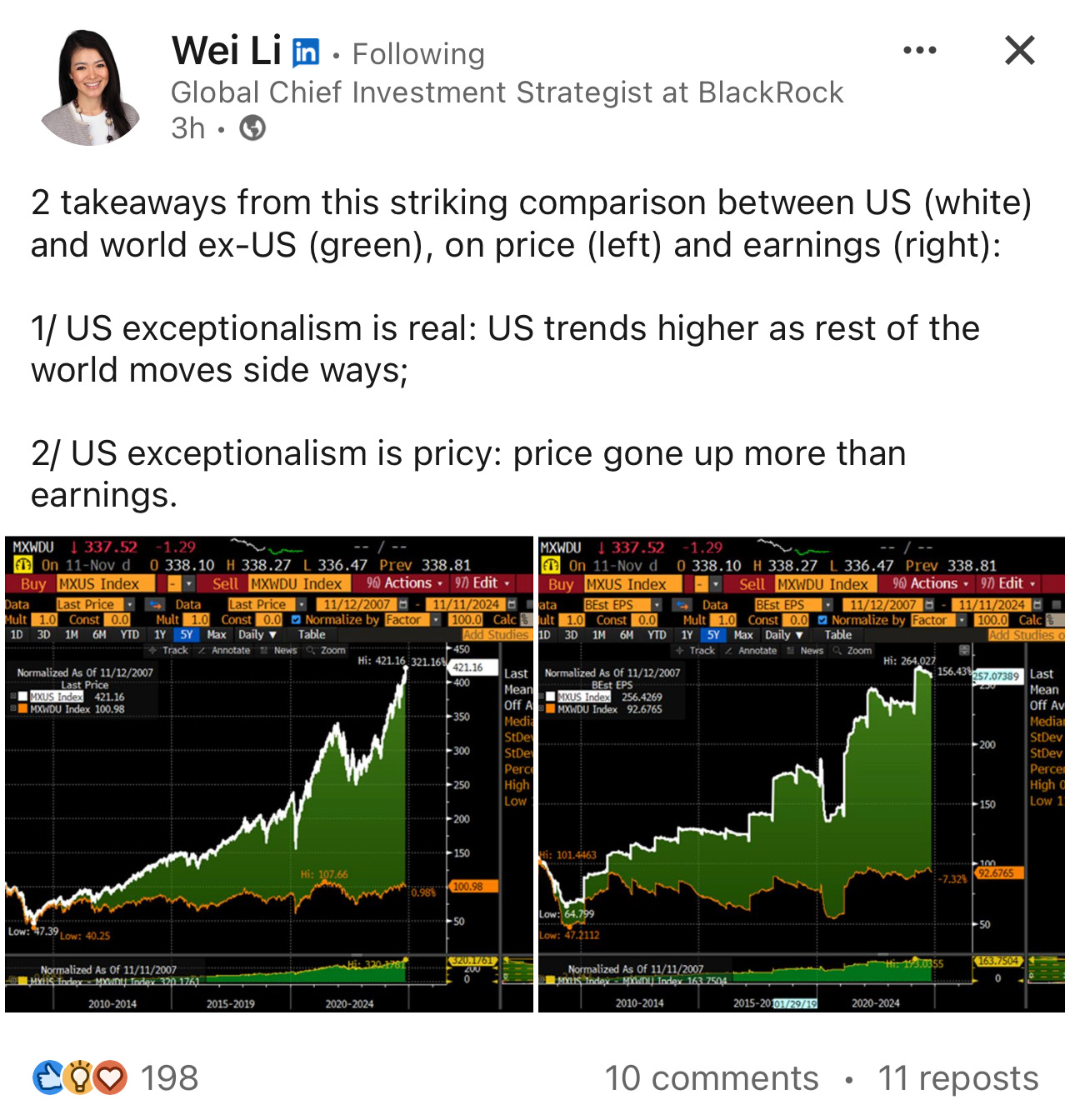

This week’s featured post highlights a compelling comparison between the performance of US equities (white) and world ex-US equities (green) since 2007, with key takeaways on the drivers behind the US’s remarkable outperformance.

US exceptionalism is real: While global markets have largely moved sideways, US equities have trended significantly higher, supported by both earnings growth and valuation expansion.

US exceptionalism is pricy: The data reveals that US outperformance is largely attributable to valuation expansion, with prices outpacing earnings growth by a wide margin.

What does this mean for investors? US equities have been the clear winners, but much of this outperformance rests on stretched valuations. Investors may want to consider balancing their portfolios with exposure to more reasonably priced global markets to manage downside risks.

Source: Wei Li - LinkedIn

💼 Market Indicators

SPY Performance

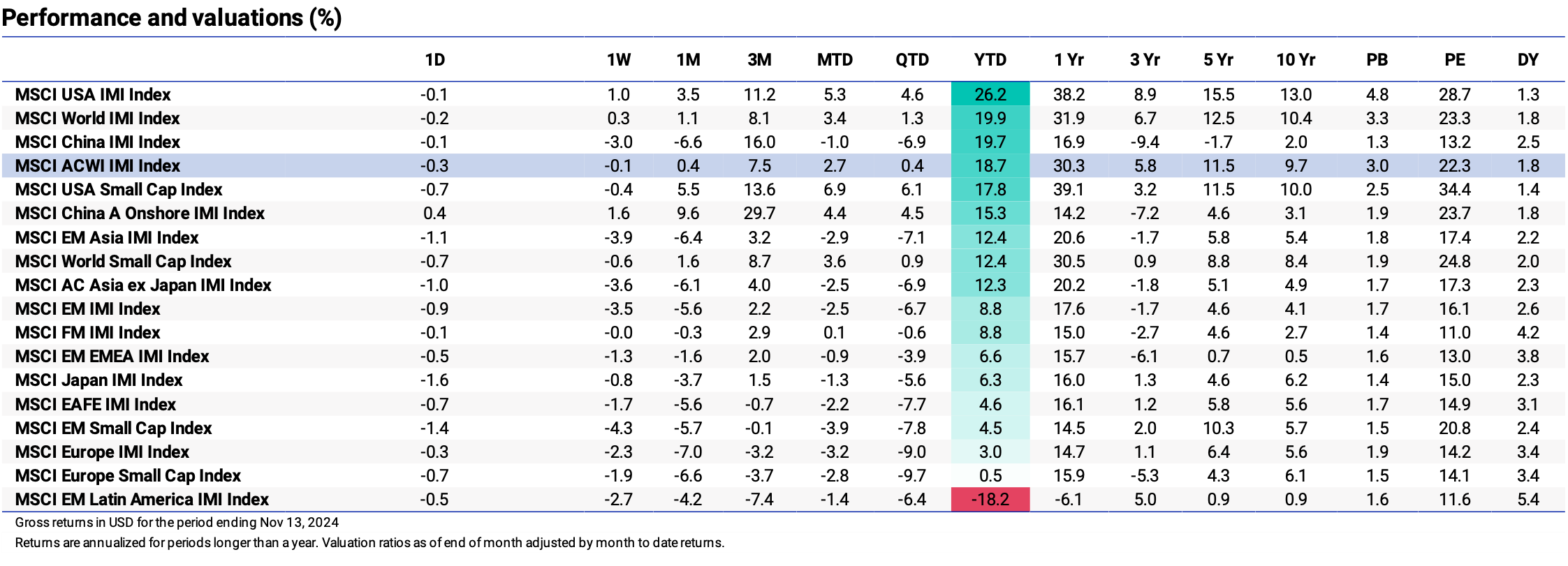

Performance and Valuations by Region

Source: MSCI

Momentum performance by Style

Source: MSCI

S&P 500 Earnings Per Share

Source: Yardeni Research

🗺️ Around the World in Detail

United States 🇺🇸: Persistent Inflation and Market Adjustments

Inflation: Headline CPI rose to 2.6% in October, while core inflation held at 3.3%, driven by rising shelter costs.

Retail Sales: Retail sales grew by 0.4% in October, exceeding expectations, with strong gains in electronics and auto sales.

Treasury Yields: The 10-year U.S. Treasury yield hit 4.51%, its highest level since June, reflecting higher-for-longer rate expectations.

International 🌐: Diverging Growth and Policy Signals

Euro Area 🇪🇺

GDP Growth: The Eurozone grew by 0.4% in Q3, its strongest performance in two years, though Germany’s growth lagged at 0.2%.

ECB Policy: Minutes from the ECB emphasized a cautious approach, with recent rate cuts described as precautionary.

Labor Market: Employment rose by 0.2% in Q3, highlighting ongoing stability despite industrial sector struggles.

United Kingdom 🇬🇧

GDP Growth: The UK economy expanded by just 0.1% in Q3, its weakest growth in three quarters, weighed down by manufacturing declines.

Unemployment: The jobless rate rose to 4.3%, its highest level since May, signaling labor market softness.

Japan 🇯🇵

GDP Growth: Japan’s economy grew by 0.2% in Q3, moderating from 0.5% in Q2, as exports underperformed.

Yen Weakness: The yen depreciated to the JPY 155 range against the dollar, pressured by expectations of inflationary U.S. policies.

Emerging Markets 🌏: Diverging Signals Across Key Economies

China 🇨🇳

Deflation Concerns: Producer prices fell 2.9% in October, deepening deflation, though retail sales grew by 4.8%, boosted by stimulus measures.

Housing: Home price declines slowed, reflecting early signs of stabilization in the property market.

India 🇮🇳

Inflation: CPI surged to 6.21% in October, breaching the RBI’s tolerance levels, driven by rising food costs.

Growth Outlook: Persistent price pressures may delay rate cuts, complicating India’s growth recovery.

South Korea 🇰🇷

Unemployment: The jobless rate rose to 2.7% in October, reflecting a softening labor market despite modest employment gains.

The content provided on MacroQuant Insights is for informational and educational purposes only and does not constitute financial advice. While every effort is made to ensure accuracy and reliability, all data, analysis, and opinions are based on sources believed to be trustworthy but are not guaranteed for completeness or timeliness. The views expressed are solely those of the author and do not reflect endorsements or recommendations for any specific investment, strategy, or action.

Investing involves inherent risks, including the potential loss of principal. Past performance is not indicative of future results. We strongly encourage readers to conduct their own research and consult with a qualified financial advisor or professional before making any financial decisions. MacroQuant Insights and its contributors disclaim all liability for investment decisions based on the information provided and make no warranties regarding the content’s accuracy or reliability.

Remember, all investments carry risks, and it is essential to understand these risks fully before acting on any information presented. Users are responsible for their own investment decisions. MacroQuant Insights assumes no responsibility for any outcomes resulting from the use of this information. Content is subject to change without notice.