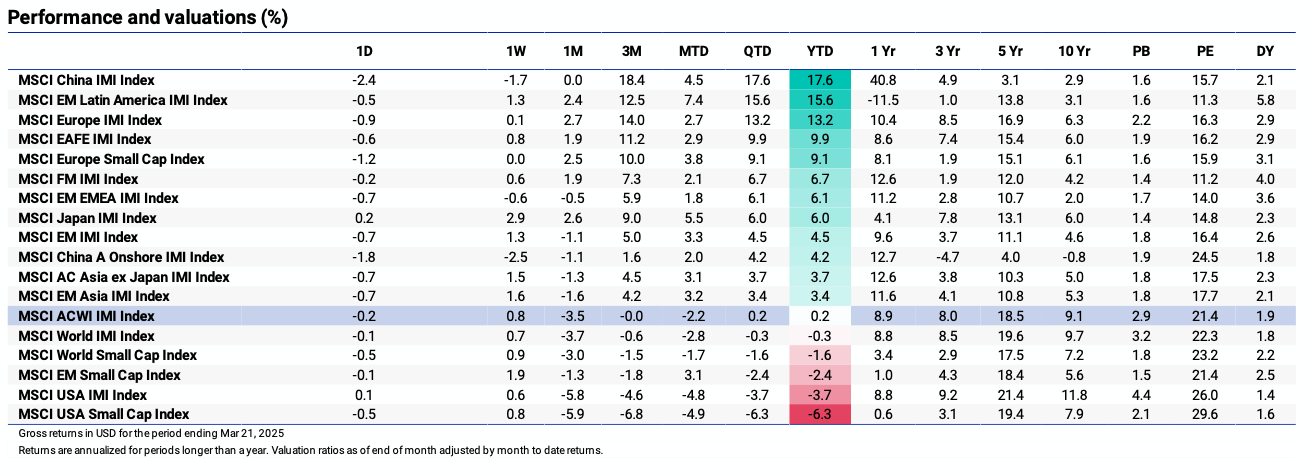

European equities have surged 10.8% year-to-date in local currency terms, while the S&P 500 has retreated 3.9% - creating a remarkable 14.7 percentage point performance gap between the regions. This divergence, fueled by defense sector strength and ECB rate cut expectations, represents one of the most significant regional rotations since the post-pandemic recovery. As U.S. markets continue to be weighed down by tech underperformance and lofty valuations, European stocks are benefiting from both a valuation advantage and sector composition that's well-positioned for the current macroeconomic environment.

⏱️ Global Markets in 10 Seconds:

🇺🇸 Fed holds at 4.25%-4.5% amid "increased uncertainty" ⚠️

🇪🇺 European stocks +10.8% YTD outperforming S&P by 14.7 points 📈

🇯🇵 BoJ remains cautious at 0.5% as inflation eases to 3.7% 🏦

🇨🇳 Unemployment rises to 5.4% highest in two years 💼

🇬🇧 BoE votes 8-1 to maintain 4.5% rate despite inflation concerns 🎯

🔍 The Big Picture

The financial markets are giving us a tale of regional divergence, with European stocks dramatically outperforming their American counterparts. This rotation away from U.S. dominance reflects shifting investor priorities from growth to value, changing central bank expectations, and sector-specific advantages that are reshaping the global investment landscape.

United States: The Fed's decision to hold rates at 4.25%-4.5% while projecting only 50 basis points of cuts for 2025 highlights their cautious stance despite acknowledging "increased uncertainty." What's particularly telling is their simultaneous downward revision of GDP growth (to 1.7% from 2.1%) and upward revision of inflation forecasts (to 2.7% from 2.5%) – signaling the sticky inflation problem isn't going away easily, even as growth moderates.

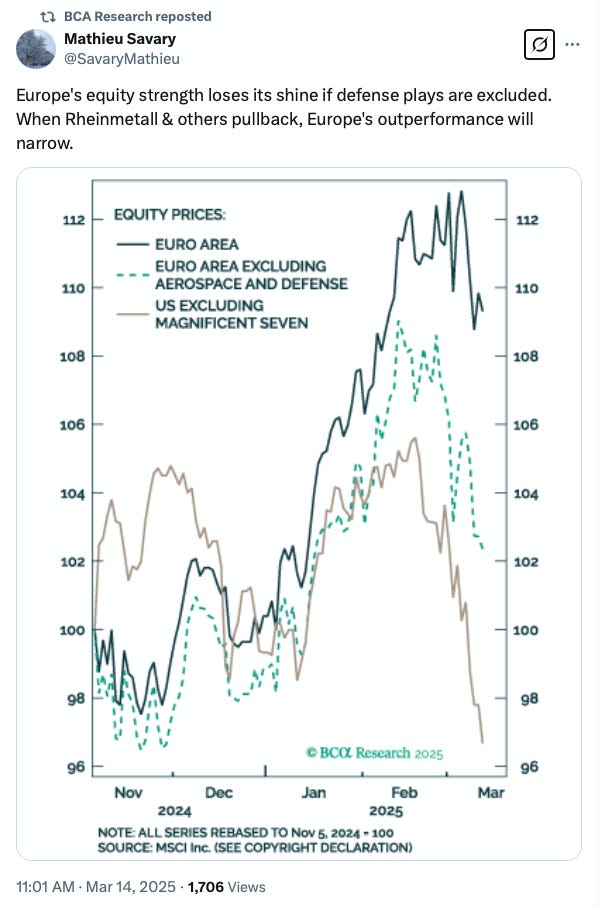

International: European equities' stunning 10.8% YTD gain versus the S&P 500's 3.9% decline represents one of the most significant regional rotations we've seen in years. Defense stocks are the unsung heroes here – strip them out (as Mathieu Savary's analysis shows) and Europe's outperformance narrows considerably. This sector advantage, combined with relative undervaluation (UK stocks trading at nearly a 50% discount to the S&P) creates a compelling value proposition that's becoming harder for global investors to ignore.

Emerging Markets: China's rise in unemployment to 5.4% (a two-year high) tells us that despite better-than-expected retail sales growth of 4.0%, structural challenges persist beneath the surface. The property sector remains a significant drag with development investment sinking 9.8% in the first two months of 2025, suggesting that even as consumption improves, the economy's foundation still has serious cracks that monetary easing alone may struggle to repair.

💼 Market Indicators

SPY Performance

Performance and Valuations by Region

Source: MSCI

Momentum performance by Style

Source: MSCI

S&P 500 Earnings Per Share

Source: Yardeni Research

🗺️ Around the World in Detail

🇺🇸 United States: Mixed Signals Ahead

Fed maintains caution: The central bank kept rates steady at 4.25%-4.5% and still projects just 50 basis points of cuts in 2025, despite acknowledging "uncertainty around the economic outlook has increased." Think of this as your cautious friend who keeps one foot on the brake even when the road looks clear ahead.

Retail disappointment: February's retail sales crawled up just 0.2%, well below the expected 0.7% rise and following January's steep 1.2% decline. The consumer engine that powers nearly 70% of the US economy might be running on fumes, though the control group sales (the part that feeds directly into GDP) jumped a surprising 1%, giving economists something to chew on.

Housing silver lining: Existing home sales rose 4.2% in February while housing starts jumped 11.2% to an annual rate of 1.5 million. Like finding unexpected growth in your garden after a long winter, the housing market is showing signs of life despite high mortgage rates, largely thanks to increased supply.

Value's winning streak: Value stocks have outperformed growth for five consecutive weeks, racking up an impressive 897 basis point advantage year-to-date. This rotation is like watching a steady marathoner finally overtake the flashy sprinter who's been hogging the spotlight.

🌐 International Markets: Europe's Surprising Strength

Canada 🇨🇦

Inflation jumped dramatically to 2.6% in February from 1.9% in January, largely due to the end of GST and HST tax breaks. Like removing a bandage, this tax credit expiration exposed the underlying inflation pressure that was there all along.

Core inflation rose for the fourth consecutive month to 2.7%, putting Canada's central bank in a tricky position after its recent dovish pivot. The Bank of Canada might need to reconsider its rate-cutting path if this trend continues.

Europe 🇪🇺

European equities have delivered a stunning 10.8% YTD return while the S&P 500 has fallen 3.9%, creating a remarkable 14.7 percentage point performance gap. This isn't just a brief moment in the sun – it's a fundamental shift that's catching many global investors by surprise.

The defense sector is Europe's secret weapon, with companies like Rheinmetall seeing substantial gains amid increased military spending. As Mathieu Savary's (BCA Research) analysis shows, if you strip out aerospace and defense stocks, Europe's outperformance narrows considerably.

UK 🇬🇧

The Bank of England held rates at 4.5% with a surprisingly hawkish 8-1 vote, when markets had expected more members to favor cuts. This cautious stance reflects ongoing concerns about sticky inflation, particularly in services.

Unemployment remained steady at 4.4%, with employment increasing by 144,000 to 33.92 million, primarily driven by growth in full-time positions. The UK labor market continues to show resilience despite economic headwinds.

Japan 🇯🇵

The Bank of Japan kept its short-term policy rate unchanged at 0.5%, taking a wait-and-see approach amid rising global economic risks. Unlike its Western counterparts, the BoJ is still in the early stages of normalizing rates after decades of ultra-loose policy.

Inflation eased to 3.7% in February from January's 4.0% two-year high, with core inflation dropping to 3.0%. This gives the BoJ breathing room to move gradually on further rate hikes.

🌏 Emerging Markets: Contradictory Signals

China 🇨🇳

Retail sales rose 4.0% year-over-year in January-February, the strongest increase since October, suggesting consumer spending is holding up better than expected. This is like finding water in a desert – a welcome sign amid challenging economic conditions.

The urban unemployment rate climbed to 5.4%, the highest level in two years, while property development investment sank 9.8%. These structural challenges are the equivalent of termites in the foundation – not immediately visible but potentially destabilizing if left unaddressed.

Taiwan 🇹🇼

Taiwan's central bank maintained its key discount rate at 2%, reflecting concerns about US trade policies and their potential impact on Taiwan's export-driven economy. Like a smaller boat in choppy waters, Taiwan must navigate carefully between major economic powers.

The central bank slightly lowered its 2025 economic growth forecast to a still-impressive 3.05%, while expecting inflation to moderate to 1.89%. Taiwan continues to outperform many of its regional peers despite heightened geopolitical tensions.

🔑 Key Takeaway

This week's data illuminates a profound regional divergence in equity markets, with European stocks outperforming their American counterparts by a staggering 14.7 percentage points year-to-date. This rotation isn't merely a statistical curiosity – it reflects a fundamental shift in market dynamics where European value-oriented sectors (particularly defense) are thriving while the tech-heavy U.S. market struggles under the weight of lofty valuations and reduced growth expectations.

The Fed's simultaneous downward revision of GDP forecasts (to 1.7% from 2.1%) and upward revision of inflation expectations (to 2.7% from 2.5%) underscores the challenging environment for growth stocks, especially as central banks diverge in their policy approaches. Savary's research highlighting the outsized contribution of defense stocks to Europe's performance reveals a crucial insight: sector composition, not just regional economics, is driving this divergence – a reminder that in today's market, understanding what's under the hood matters far more than the brand name on the vehicle.

The content provided on MacroQuant Insights is for informational and educational purposes only and does not constitute financial advice. While every effort is made to ensure accuracy and reliability, all data, analysis, and opinions are based on sources believed to be trustworthy but are not guaranteed for completeness or timeliness. The views expressed are solely those of the author and do not reflect endorsements or recommendations for any specific investment, strategy, or action.

Investing involves inherent risks, including the potential loss of principal. Past performance is not indicative of future results. We strongly encourage readers to conduct their own research and consult with a qualified financial advisor or professional before making any financial decisions. MacroQuant Insights and its contributors disclaim all liability for investment decisions based on the information provided and make no warranties regarding the content’s accuracy or reliability.

Remember, all investments carry risks, and it is essential to understand these risks fully before acting on any information presented. Users are responsible for their own investment decisions. MacroQuant Insights assumes no responsibility for any outcomes resulting from the use of this information. Content is subject to change without notice.