The European Central Bank slashed interest rates by 25 basis points to 2.25% this week, marking its seventh consecutive cut since last summer amid escalating global trade tensions. This monetary easing, driven by the ECB's concerns about deteriorating growth prospects and confidence that inflation is returning to target, stands in stark contrast to the holding patterns at the Federal Reserve, Bank of Canada, and Bank of Korea. While European policymakers pivot toward supporting economic growth, Federal Reserve Chair Jerome Powell emphasized that unexpectedly large tariff increases would likely slow growth and raise inflation, creating a precarious balancing act for central banks worldwide.

⏱️ Global Markets in 10 Seconds:

🇺🇸 Retail sales +1.4% highest in two years as consumers rush ahead of tariffs 🛒

🇪🇺 ECB cuts to 2.25% amid trade war uncertainty, 7th consecutive reduction 🏦

🇨🇳 GDP grows 5.4% exceeding expectations despite looming tariff impacts 📈

🇬🇧 Inflation eases to 2.6% as falling fuel prices offset housing costs 💰

🇯🇵 Exports slow to 3.9% as trade tensions with US intensify ⚠️

🔍 The Big Picture

Central banks are diverging in their policy responses to the escalating global trade war, creating a fascinating laboratory for how different monetary approaches perform under similar external pressures. While some are prioritizing growth concerns, others remain focused on inflation risks, highlighting the fundamental tradeoff that defines central banking in uncertain times.

United States: Retail sales jumped 1.4% in March, the strongest gain in over two years, with auto sales surging 5.3% as consumers rushed to beat tariff-driven price increases. This represents a pull-forward of demand that boosts current numbers but potentially at the expense of future consumption, creating temporary strength that might mask underlying weakness.

Europe: The ECB's decision to cut rates to 2.25% stands in stark contrast to the Bank of Canada's pause at 2.75% and the Fed's holding pattern. This divergence highlights different policy priorities – the ECB is addressing growth concerns more aggressively while others are still primarily focused on inflation risks.

Emerging Markets: China's surprising 5.4% GDP growth in Q1 arrived just as new tariffs threaten to reshape global trade flows. The Chinese economy demonstrated impressive momentum in early 2025, but now faces significant headwinds that could require additional stimulus to maintain growth targets.

💼 Market Indicators

SPY Performance

Performance and Valuations by Region

Source: MSCI

ACWI Momentum performance by Style

Source: MSCI

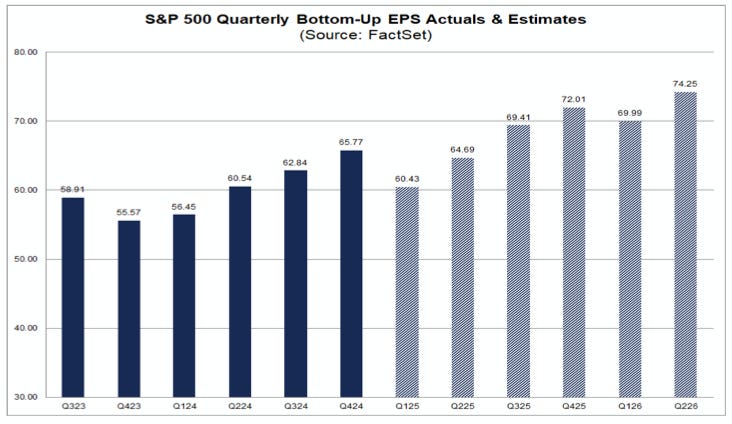

S&P 500 Earnings Per Share

Source: Yardeni Research

Source: FactSet

🗺️ Around the World in Detail

🇺🇸 United States: Consumption Contradiction

Retail sales surged 1.4% in March, the strongest gain in over two years. This represents consumers accelerating purchases, with auto sales jumping 5.3% as buyers rushed to beat tariff-driven price increases.

Housing starts plunged 11% to 1.32 million annualized units in March, missing expectations by a wide margin. Developers are pausing construction plans as they struggle to accurately forecast project costs when they don't know how much materials will cost after tariffs take effect.

Fed Chair Powell acknowledged the economic impact of tariffs will include "higher inflation and slower growth," while indicating the Fed is "well positioned to wait" before adjusting rates. The central bank is carefully evaluating incoming data before making policy changes.

🌐 International Markets: Divergent Strategies

Canada 🇨🇦

Bank of Canada held rates at 2.75% after seven consecutive cuts, citing "unpredictability on the magnitude of tariffs." The BoC is pausing to assess how trade tensions will affect the economic outlook.

Inflation cooled to 2.3% in March from 2.6% in February, a welcome development that provides the BoC with additional flexibility. This improvement gives policymakers more room to respond to changing conditions.

Europe 🇪🇺

ECB cut rates by 25bps to 2.25%, its seventh consecutive reduction, amid growing confidence inflation is returning to target. European policymakers are moving more aggressively than their counterparts in North America.

The central bank acknowledged that "growth prospects have weakened" due to rising global trade tensions, which are "hurting confidence and tightening financial conditions." The ECB sees deteriorating economic conditions requiring proactive policy intervention.

UK 🇬🇧

Inflation eased to 2.6% in March from 2.8%, falling below both market and BoE forecasts of 2.7%. This gradual improvement provides the BoE with greater flexibility in considering rate cuts.

Unemployment remained steady at 4.4% for the fourth consecutive period, while employment rose by 206,000 to a record high of 34 million. The UK labor market continues to demonstrate remarkable resilience despite broader economic uncertainties.

Japan 🇯🇵

Export growth slowed sharply to 3.9% year-on-year in March from 11.4% in February, as U.S. steel and aluminum tariffs began to bite. This is the canary in the coal mine for Japan's export-dependent economy.

Inflation edged down to 3.6% in March from 3.7%, while core inflation rose to 3.2% from 3.0%. The BoJ is walking a tightrope – trying to normalize monetary policy while watching trade tensions threaten their export-oriented growth model.

🌏 Emerging Markets: Resilience Testing

China 🇨🇳

GDP grew 5.4% year-on-year in Q1, maintaining the same pace as Q4 and exceeding expectations of 5.1%. China's economy has performed well thus far, but now faces significant new challenges.

Retail sales jumped 5.9% in March from 4% in January-February, the strongest reading since December 2023. Chinese consumers are showing surprising strength, but questions remain whether this can continue as trade tensions escalate.

India 🇮🇳

Inflation fell to 3.34% in March, the lowest since August 2019 and the fifth consecutive monthly decline. India has achieved an enviable balance maintaining growth without significant inflationary pressure.

Food inflation, which accounts for nearly half of India's price basket, dropped to a near four-year low of 2.69%, providing relief to consumers. This represents a significant improvement in a critical component of the country's inflation basket.

South Korea 🇰🇷

Bank of Korea maintained its base rate at 2.75% following a 25bps cut in February, aligning with market expectations. Korean policymakers are taking a measured approach to monetary policy.

The central bank slashed its 2025 growth forecast to below 1.5% from 1.5%, citing U.S. tariff policy changes and domestic political uncertainty. This downgrade highlights that even strong economies are vulnerable to global trade disruptions.

🔑 Key Takeaway

This week's data paints a vivid picture of central bank divergence amid escalating trade tensions. The ECB's decisive cut to 2.25% contrasts sharply with the Fed and BoC's holding pattern, highlighting how policymakers weigh the same challenges but reach different conclusions about whether inflation or growth poses the greater risk. American consumers rushed to beat tariffs with retail sales jumping 1.4%, while China's strong 5.4% GDP growth now faces significant headwinds as new tariffs reshape global trade.

The tension between economic resilience and policy uncertainties creates both risks and opportunities, particularly in currency and fixed-income markets where these divergences are directly priced. Think of it as sailing in waters where different weather systems are colliding – you need to understand both current conditions and how they might shift when these systems interact. Investors who correctly assess which central bank's diagnosis proves right will find themselves with significant advantage in positioning across asset classes.

The content provided on MacroQuant Insights is for informational and educational purposes only and does not constitute financial advice. While every effort is made to ensure accuracy and reliability, all data, analysis, and opinions are based on sources believed to be trustworthy but are not guaranteed for completeness or timeliness. The views expressed are solely those of the author and do not reflect endorsements or recommendations for any specific investment, strategy, or action.

Investing involves inherent risks, including the potential loss of principal. Past performance is not indicative of future results. We strongly encourage readers to conduct their own research and consult with a qualified financial advisor or professional before making any financial decisions. MacroQuant Insights and its contributors disclaim all liability for investment decisions based on the information provided and make no warranties regarding the content’s accuracy or reliability.

Remember, all investments carry risks, and it is essential to understand these risks fully before acting on any information presented. Users are responsible for their own investment decisions. MacroQuant Insights assumes no responsibility for any outcomes resulting from the use of this information. Content is subject to change without notice.