Canadian markets faced a pivotal shift this week as the Bank of Canada slashed its key interest rate by another 50 basis points, marking a cumulative 175 bps reduction this cycle. This move, driven by slowing GDP growth of 1.0% annualized in Q3 and mounting risks of a Q4 miss, signaled a cautious path ahead for policymakers. While inflation remains near the 2% target, the BoC’s restrained outlook for 2025 suggests that tighter borrowing conditions continue to weigh heavily on economic momentum.

As Canada recalibrates its policy stance, the implications for growth and global rate expectations underscore a growing divergence among central banks entering the new year.

⏱️ Global Markets in 10 Seconds:

🇺🇸 242K jobless claims point to a cooling labor market 💼

🇪🇺 ECB cuts rates to 3% as growth stagnates at PMI 47.8 🏦

🇨🇳 CPI at 0.2% signals persistent deflation risks ⚠️

🇨🇦 BoC slashes 50bps as GDP slows to 1% annualized 📉

🇮🇳 Inflation eases to 5.48%, growth remains resilient 🚀

🔍 The Big Picture

Global markets reflected diverging economic conditions this week, with central banks in Canada and Europe cutting rates to combat slowing growth while the U.S. edged closer to another Fed rate cut. Emerging markets showcased contrasting dynamics, as India’s resilience stood in stark contrast to China’s lingering deflation risks

United States: Core inflation held steady at 3.3% in November, while jobless claims jumped to a two-month high of 242,000, signaling a cooling labor market. These data points bolstered expectations for a Fed rate cut, with market pricing now showing a 97% probability. Meanwhile, the Nasdaq climbed above 20,000 for the first time, driven by tech gains, as Tesla rose 12.08% and Alphabet surged 8.44%.

International: Europe’s 25 bps ECB rate cut and a surprise 50 bps SNB cut underscored central banks’ focus on supporting sluggish growth, as Eurozone PMI contracted to 47.8. In the UK, the economy shrank 0.1% in October, with flat services output and a 0.6% drop in manufacturing highlighting broad weakness. Japan outperformed expectations, with GDP rising 0.3% in Q3, while speculation about a BoJ hike delay weighed on the yen.

Emerging Markets: India’s inflation eased to 5.48%, opening the door for potential rate cuts as food prices cooled sharply. In contrast, China’s CPI grew just 0.2%, heightening deflation risks, while exports slowed to 6.7% in November from 12.7% the prior month. South Korea’s unemployment held steady at 2.7%, reflecting resilience, though broader export-driven growth challenges persist in the region.

⭐️ Post of the week

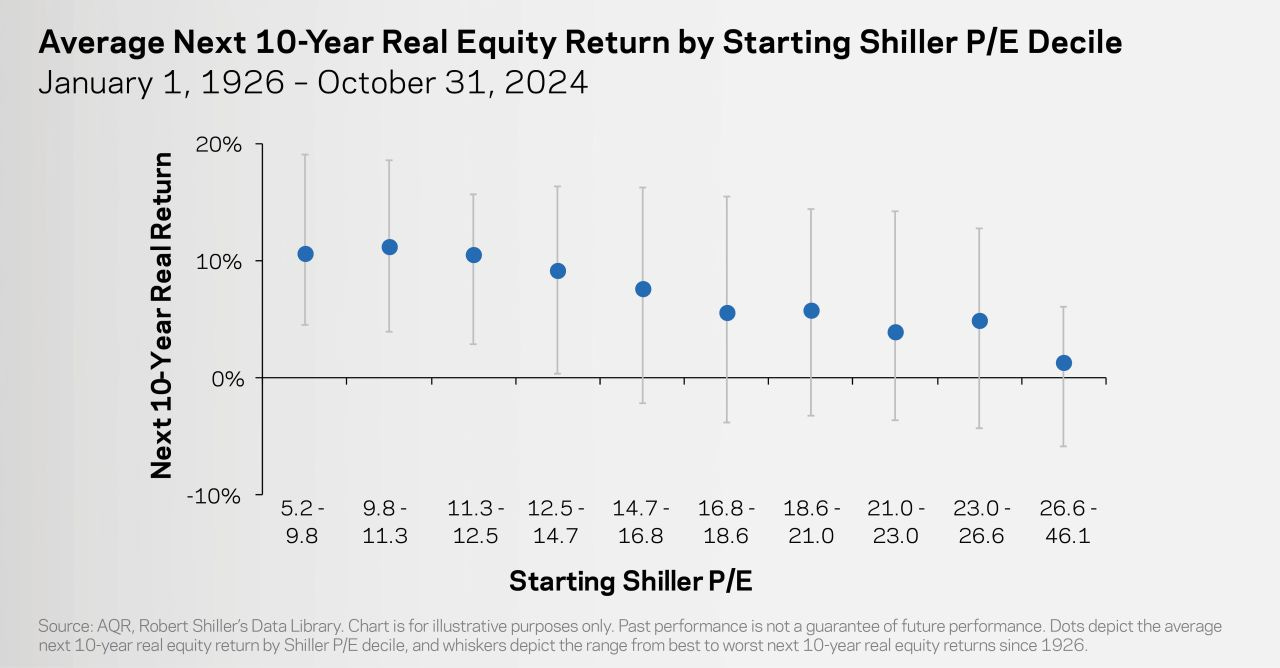

This week, AQR Capital Management highlighted the critical relationship between high equity valuations and future returns, using the Shiller P/E ratio as a key measure. Their analysis challenges the assumption that strong past returns ensure continued growth, instead revealing how expensive markets can lead to muted long-term performance.

Why This Analysis Matters

• The Shiller P/E Framework: The Shiller P/E (price-to-earnings over a 10-year period) is a widely used tool to smooth out earnings volatility and gauge equity market valuation. AQR’s chart links today’s P/E levels to the potential real equity returns over the next decade.

• Challenging Market Optimism: With U.S. P/E levels at 37, their third-highest in history, the data underscores the inverse relationship between elevated valuations and future returns—a stark reminder that markets don’t always reward prolonged optimism.

• Structural Insight Over Simplicity: Instead of relying on short-term momentum, this approach connects valuation extremes to structural market outcomes, reinforcing the need for investors to consider long-term risk-adjusted returns in portfolio construction.

Supporting Evidence

• Last week’s data showed U.S. P/E ratios remain at decade-high levels, surpassing all but the Tech Bubble (46) and pre-2021 peak (40). Historical data suggests that starting valuation extremes are often followed by lower real returns over 10 years.

• The chart demonstrates that when the Shiller P/E reaches the top decile (26.6+), average next 10-year real returns drop to near 0%, compared to the 10%-plus averages seen at lower valuation levels. This challenges complacent assumptions in current market optimism.

• While surface-level market strength may appear encouraging, AQR’s analysis reveals how valuations remain structurally stretched, even as returns have outpaced earnings. This disconnect underscores the importance of valuation as a forward indicator.

Bottom Line

This analysis is a clear reminder that valuation levels matter for long-term returns. Investors can improve their process by integrating tools like the Shiller P/E into their framework, challenging assumptions, and focusing on risk-adjusted opportunities rather than chasing past performance.

Source: AQR Capital Management - LinkedIn

💼 Market Indicators

SPY Performance

Performance and Valuations by Region

Source: MSCI

Momentum performance by Style

Source: MSCI

S&P 500 Earnings Per Share

Source: Yardeni Research

🗺️ Around the World in Detail

United States 🇺🇸: Rate Cuts on the Horizon

Core Inflation Steady at 3.3%: Inflation held firm in November, driven largely by shelter costs, which rose 0.3% and accounted for nearly 40% of the monthly increase. With inflation showing no signs of a further cooldown, markets remain laser-focused on next week’s Fed decision.

Jobless Claims Hit 242,000: Weekly claims jumped to a two-month high, pointing to a labor market that is cooling but not collapsing. This aligns with the Fed’s soft-landing narrative and reinforces expectations of a rate cut in early 2025.

Nasdaq Crosses 20,000: While most major indices dipped, tech stocks surged, with Tesla rising 12.08% and Alphabet posting its strongest gains since 2015. Growth continues to dominate as investors weigh rate cuts and slowing economic momentum.

International 🌐: Central Banks Ease Up

Canada 🇨🇦

BoC Cuts Rates by 50 bps: The Bank of Canada delivered its second consecutive 50-basis-point cut, bringing rates down to 4.25%. Policymakers emphasized caution for next year, signaling a pause in further cuts amid uncertainties over U.S. trade policies.

GDP Misses Expectations: Growth slowed to 1% annualized in Q3, below forecasts. The risk of a fourth-quarter contraction looms, even as consumer spending holds up better than expected.

Euro Area 🇪🇺

ECB Cuts Rates to 3%: The European Central Bank eased policy for the fourth time this year, citing a softer inflation outlook. With growth expected at just 0.7% in 2024, the ECB left room for more cuts in 2025 to stabilize sluggish economies.

Eurozone PMI at 47.8: Manufacturing continues to contract, with Germany struggling to offset broader regional weakness. This highlights the delicate balancing act for European policymakers as they seek growth without reigniting inflation.

United Kingdom 🇬🇧

Economy Contracts 0.1%: October GDP data showed the second straight monthly decline, driven by a 0.6% drop in manufacturing output. Flat services growth reflects weakening demand, pressuring the Bank of England to maintain its cautious stance.

Japan 🇯🇵

GDP Beats Expectations: The economy grew 0.3% in Q3, surpassing forecasts, as business investment contracted less than anticipated. However, speculation about a delayed BoJ rate hike pushed the yen lower, boosting Japanese equities.

Emerging Markets 🌏: Diverging Paths

China 🇨🇳

Inflation Stuck at 0.2%: Persistent deflation risks remain, despite government pledges for proactive fiscal policies and infrastructure spending. Weak consumer demand continues to challenge China’s recovery narrative.

Exports Slow to 6.7%: After a strong October, export growth moderated, partly due to firms frontloading shipments to the U.S. ahead of potential tariffs. Global demand uncertainty looms for 2025.

India 🇮🇳

Inflation Falls to 5.48%: Food prices cooled sharply, bringing inflation back within the RBI’s target range. This could pave the way for rate cuts in 2025, reinforcing India’s position as the region’s growth leader.

Economic Momentum Holds: Strong domestic demand continues to underpin India’s resilience, even as global trade faces headwinds.

South Korea 🇰🇷

Unemployment at 2.7%: Jobless rates remained steady, reflecting labor market stability. However, concerns about global trade persist as South Korea navigates a slowing export environment.

Taiwan 🇹🇼:

Quiet on Growth: With no major updates this week, Taiwan remains steady as global tech demand holds the key to its near-term economic trajectory.

🔑 Key Takeaway

This week's data highlights a global economy grappling with slowing momentum and diverging policy responses. While the Bank of Canada and ECB delivered rate cuts to counter sluggish growth—underscored by Canada’s 1% GDP and Eurozone PMI at 47.8—the U.S. labor market softened further, with jobless claims rising to 242,000. Meanwhile, China’s lingering deflation risks, with CPI at just 0.2%, contrasted sharply with India’s resilient inflation cooldown to 5.48%, positioning it for continued strength. These trends signal a shifting monetary landscape as central banks balance growth concerns against inflation targets, with clear implications for investor positioning heading into 2025.

The content provided on MacroQuant Insights is for informational and educational purposes only and does not constitute financial advice. While every effort is made to ensure accuracy and reliability, all data, analysis, and opinions are based on sources believed to be trustworthy but are not guaranteed for completeness or timeliness. The views expressed are solely those of the author and do not reflect endorsements or recommendations for any specific investment, strategy, or action.

Investing involves inherent risks, including the potential loss of principal. Past performance is not indicative of future results. We strongly encourage readers to conduct their own research and consult with a qualified financial advisor or professional before making any financial decisions. MacroQuant Insights and its contributors disclaim all liability for investment decisions based on the information provided and make no warranties regarding the content’s accuracy or reliability.

Remember, all investments carry risks, and it is essential to understand these risks fully before acting on any information presented. Users are responsible for their own investment decisions. MacroQuant Insights assumes no responsibility for any outcomes resulting from the use of this information. Content is subject to change without notice.